Digital Disruption in the Banking Industry: Have you Defined your QA Strategy?

Before we get there, we need to understand what is causing the whole turmoil and disruption in the banking industry.

Yes, you guessed it right. It is FinTech. But what really is FinTech?

Per Wiki, ‘Financial technology, also known as FinTech, is an economic industry composed of companies that use technology to make financial services more efficient. Financial technology companies are generally startups founded with the purpose of disrupting incumbent financial systems and corporations that rely less on software.’

In essence, FinTech is how technology has made its presence felt in the Banking Industry.

The Risk of Disruption

Today’s highly-active-on-the-social-media users are very different from the past generations. They don’t like to wait much – and anything that helps them perform a task in an ‘anytime, anywhere’ mode catches there attention really quick. This is the sum total of the challenge that the banking and financial industry is facing today.

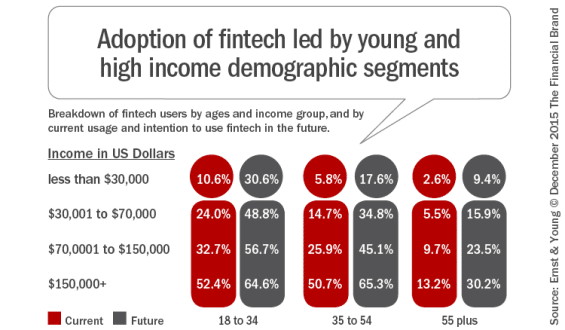

According to EY’s first FinTech Adoption Index, the average FinTech users are young, urban and belong to a higher-income group.

Imran Gulamhuseinwala, EY Global FinTech Leader, said, “The adoption of FinTech products is relatively high…, so the risk of disruption is real.”

Add to this the availability of so many apps that need to perform on so many different mobile devices that use so many different OSs – and there the banking industry has another huge Mobile-related Goliath to slay.

The Solution

Per Jim Marous, Co-Publisher of The Financial Brand and Publisher of the Digital Banking Report, “It is time for banks to take the FinTech movement seriously as adoption of FinTech could double among digitally active consumers in 2016.”

It is only obvious that both the rate of technology growth and the number of digitally active users is going to increase multifold. Financial institutions that still operate in a traditional manner will need to invest a lot in understanding these latest demands of their consumers and implement changes and strategies to improve their innovation, communication, and product development.

These organizations will need to come up with new and contemporary digital strategies to appeal to the younger consumers, as also retain the existing consumers.

“These organizations will have to review how their offerings, such as their own multi-channel strategies or partnerships with FinTech providers, meet their customers’ needs. Otherwise, they may have difficulty stemming the flight to FinTech”, observed Steven Lewis, EY Global Lead Banking Analyst.

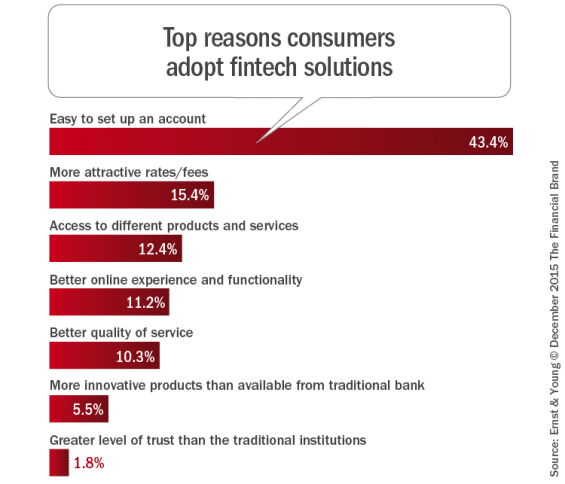

What do these institutions need to provide that will attract and retain clients? The top solution is to make their offerings and services easier to use, which in turn will make a lot of lives easier.

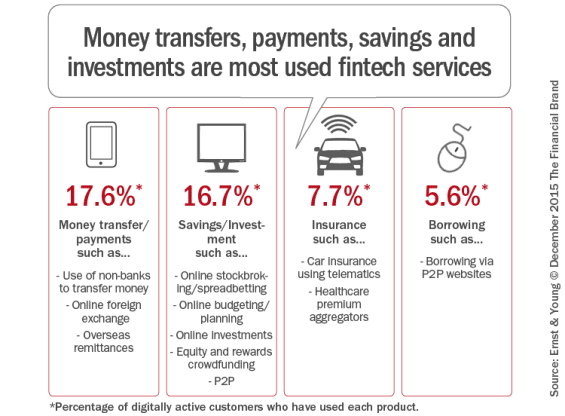

According to EY, clients also want to use the additional types of financial services when they are on the move:

The moment these organizations understand the importance of making lives easier (- read reduced paperwork and number of personal trips to banks) for their clients, they will see a lot of the challenges being overcome. To top it up, they can also provide better access to other products and services.

In short, if these organizations can provide the following similar services as by the FinTech industry, they will be able to tread on the path to better ROIs and success:

To overcome these challenges, traditional financial service providers may choose to develop partnerships with FinTech providers, or with independent software testing service specialists who can help them test the software and apps that have been built in-house.

Cigniti has a rich history of providing testing services to banking and financial institutions. Listen to the replay of this thought provoking webinar to learn how Cigniti & Experitest can help you assure software quality and succeed in the digital age to provide world class experience to Mobile Banking customers and contact us at Cigniti if you have any questions.

Leave a Reply