How Blockchain is Solving the Pain Points in the Payments Sector

Digital security has always been an issue for payment organizations and their customers. Transparent and immediate payment is the basic need. Payments need to be made easy, fast, and highly secure to enhance and popularize digital payments and be more customer-focused.

Blockchain technology has developed a solution that addresses payment security needs and transaction transparency and boosts the overall efficiency of financial transactions. The technology works on a no-intermediaries method that excludes the need for a primary regulator.

To understand this better, let us deep dive into a payment use case, its pain points, and how the blockchain payment system solves them.

Use Case – Peer-to-Peer border transaction

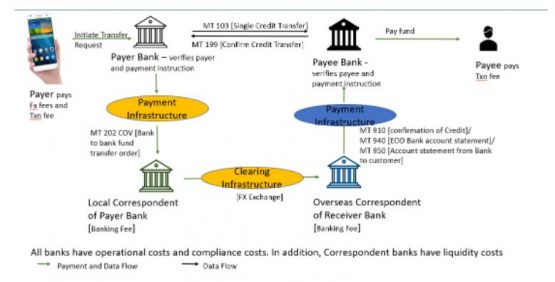

Below is the conventional flow where there is the Payer, Payer Bank, local payment infrastructure, local correspondent of payer bank, clearing infrastructure, overseas correspondent of receiver bank, receiver side payment infrastructure, payee bank:

As you can see from the above, cross-border payments are inherently more complex than domestic payments.

The Main Challenges in these Cross-Border Payments

- Transaction Speed

It takes three to five business days to complete a cross-border transaction. A significant time zone difference between the two involved currency jurisdictions plays a vital role.

To settle each currency leg, the funds need to be transferred through the relevant domestic payment systems, and the operating hours of these domestic payment systems may vary across international time zones, hence delaying the settlement of the transactions.

- Transaction Cost

Sending an international payment through the existing banking channels is a complex, multi-step process that involves several intermediaries. Cross-border payments become expensive because banks often do not have direct relationships with one another globally. They, in turn, have intermediary banks to make indirect fund transfers.

The intermediary bank charges a fee for this service, which is deducted from the total transfer amount. The remitter and the beneficiary incur this cost, or either party must pay the complete amount. This fee is on top of the fees charged by the remitter or recipient bank.

The charge is usually 2% to 3% for high-volume cross-border payments. However, it can go up to 10% if payment volumes and values are low.

- Transaction Security

Different jurisdictions have different regulatory requirements, which introduce risk to a transaction. Additionally, when records are kept by each central authority participating in the transaction, like a bank, they are vulnerable to interference.

Users could compromise their data if that authority is hacked, damaged, or taken offline.

- Transaction Opacity

Since there are multiple participants in a single transaction, tracking the payment while it is in transit is complex. There is uncertainty about the final payment amount and scheduled delivery. It is also difficult to quickly track transactions with problems.

This is due to the lack of an end-to-end system or rule set and the need to transact in different currencies across different time zones and comply with regulatory requirements.

- Correspondent banking

The number of correspondent banking relationships is declining, particularly where transaction volumes do not justify the bank’s compliance costs and in jurisdictions where transactions may be high risk or where compliance is difficult to meet.

- Liquidity

Businesses or financial institutions could also face liquidity challenges, with amounts sitting in nostro or vostro transactional accounts around the world, tying up the capital that could be used in more beneficial ways.

Now, with blockchain for payments, the above challenges are resolved.

Cross-Border Implementation with Blockchain

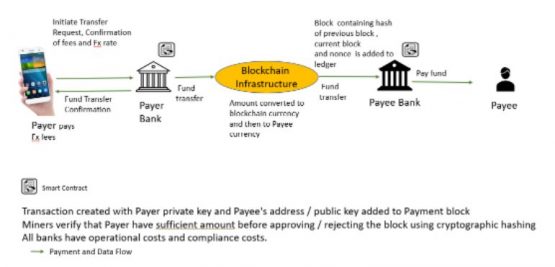

If you see the depiction below for cross-border implementation with blockchain, we only have the payer, payer bank, blockchain payment processing infrastructure, and payee bank.

-

- Transaction Speed

Blockchain payments are completed in near to real-time – in seconds rather than days. The ability to transfer money instantaneously helps businesses be more responsive, acting on or addressing customer needs without waiting for funds to come through.

- Transaction Cost

Eliminating the need for intermediaries reduces the fees for sending cross-border payments. The fees paid by transacting parties are now limited to charges imposed by the distributed ledger technology-based solution operator. Companies using blockchain in payment processing only need to pay a nominal fee, which is almost nothing.

- Transaction Security

With a blockchain payment system, all transaction records are secured by cryptography, tied to previous transactions, and distributed among participants through a ledger. A channel-based private and closed communication is laid down among the participants (buyers, sellers, and peers) to endorse, validate, and commit transactions.

Network participants have their private keys, which act as digital signatures, assigned to their transactions. If a record is altered, then the digital signature becomes invalid. This results in the peers identifying that something has occurred.

Since blockchain is decentralized and operates across a peer-to-peer network, the ledger is updated and synched amongst the participants. It means that there is no single point of failure across the ledger, and changing its state is almost impossible.

Altering the data stored on the blockchain requires permission from up to 51% of the participants simultaneously. Also, it requires enormous computing power to compromise the network. To tamper with the data, a hacker must alter all earlier transactions in the ledger.

- Transaction Transparency and Visibility

In a public blockchain solution, while a user’s identity is hidden, each address’s transactions are open to view. With an explorer and a public address, individuals, auditors, and regulatory authorities can view all transactions carried out by that address.

On the other hand, in a private blockchain solution, the details are only viewable by allowed participants involved in a transaction. All business logic is programmed as smart contracts on the network. All acknowledgments are captured as events, so there is complete transaction transparency and visibility.

- Data Integrity

Blockchain eliminates the risk of discrepancies in record keeping. As a decentralized ledger, it holds a verifiable and irreversible record of every transaction and distributes it to all authorized users. The ledger is maintained and updated communally by a group of connected computers, and all parties have an identical copy of the ledger.

The use of distributed ledgers reduces data discrepancies, facilitates quicker reconciliation, and eliminates or reduces prolonged back-office activities. Compliance is also simplified in a distributed ledger system.

- Encourages competition and innovation

The emergence of blockchain technology and blockchain-based payment firms has pressured existing cross-border payment institutions. This healthy competition will lead to innovation, which will benefit end users.

- Immune to censorship by a central governing body

In peer-to-peer blockchain architecture, there is no strict control of a central governing body as of date, which is advantageous for such global transactions. Also, banks or governments cannot drain or freeze virtual currency wallets today.

From the above, we can see that implementing blockchain for cross-border peer-to-peer payments solves the pain points of the use case. All the major pain points discussed above and how they are being solved by blockchain are tabularized below.

Pain Points of the Payment Industry How Blockchain is solving it Takes one to five days for successful transaction processing Real-time payments Multiple intermediaries create friction and bottlenecks Zero Intermediaries Expensive due to Commissions Reduced Remittance cost to 2-3% of total amount Some service providers charge a 2 to 3% fee Reduced cost Lack of transparency A high degree of transparency Save information which might not seem safe Security concerns have been addressed since the decentralized Denial of Service attack Immune to Denial of Service attacks Difficulty to support conversion to native currencies Ease of currency conversion No Cross-border payments in case of the availability of correspondent banks No geographical limitations Conclusion

Trust and transparency are the keys to payment transactions, and blockchain provides the same. However, enterprises adopting blockchain deal with privacy and security concerns, fear about the blockchain integration process, integration challenges with legacy systems, high energy consumption, and high initial investments.

By enabling real-time, cross-border payments with reduced friction and expedited settlement, blockchain empowers financial institutions to deliver enhanced customer experiences and drive financial inclusion for the unbanked.

Cigniti is one of the few IT service providers to have invested in a couple of its blockchain sandboxes across Hyperledger Fabric and R3 Corda technologies. These sandboxes are designed to quickly create a viable prototype for any business application, providing a ready environment to test the concept’s viability and its configuration’s effectiveness.

Cigniti offers targeted testing services for applications that include comprehensive validation methods across API testing, functional and non-functional testing, integration testing, security testing, compliance testing, and performance testing, and also includes specialized testing features, such as peer/node testing and smart contract testing.

Cigniti’s blockchain application testing services employ a comprehensive framework to evaluate the quality and security of blockchain-based applications rigorously. By implementing cutting-edge tools and methodologies, Cigniti’s experts ensure these transformative blockchain solutions’ seamless integration, scalability, and resilience, empowering clients to grow securely.

As the future of payments is becoming more secure and seamless, Cigniti’s expertise in blockchain testing helps clients solve complexities and capitalize on the immense potential of this disruptive technology.

Need help? Schedule a discussion with our Blockchain Testing experts to learn more about Hyperledger Fabric and R3 Corda, identify the typical blockchain project’s issues, and how Cigniti can help make the blockchain compliant.

Leave a Reply